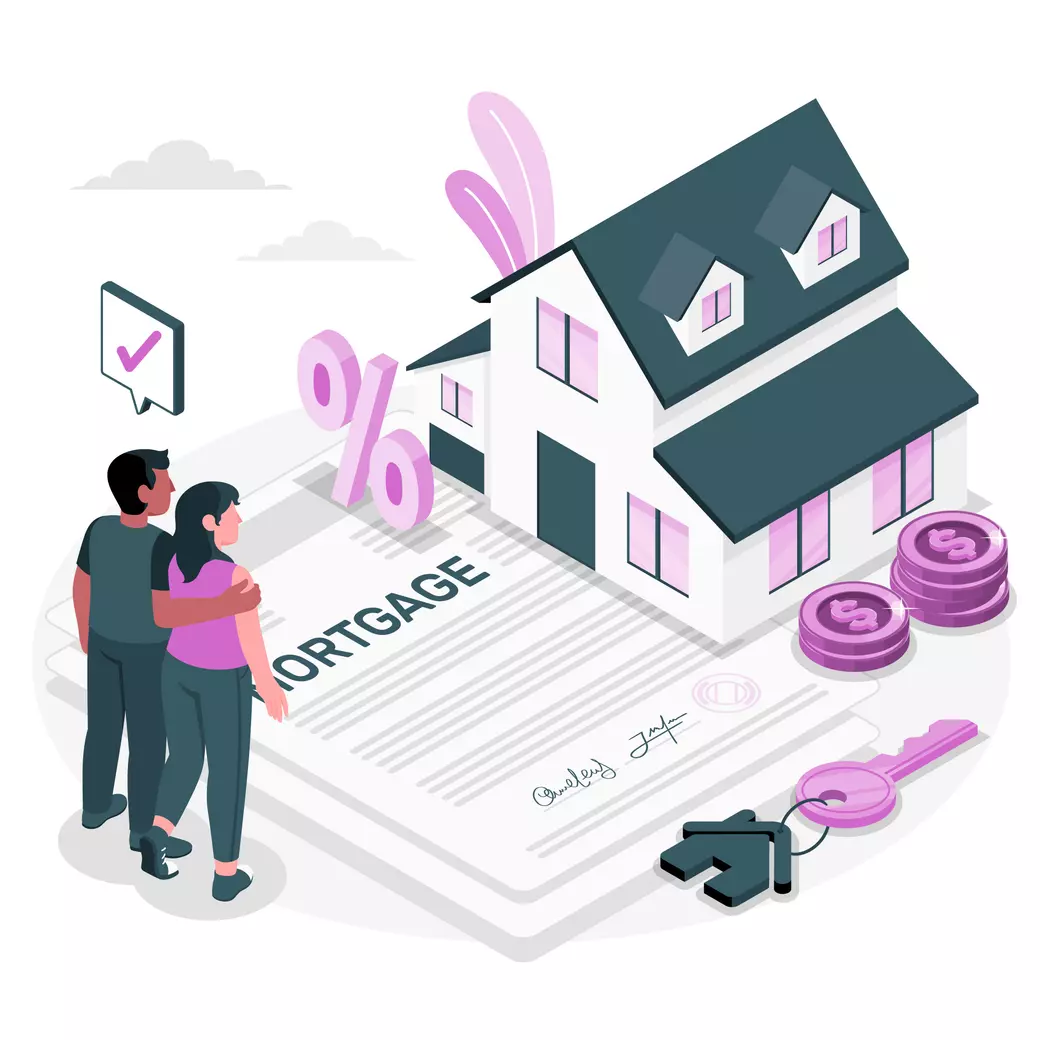

The Mortgage Process

Purchasing a home can be one of the most significant investments you'll make in your lifetime. With so much money involved, it's important to get familiar with the mortgage process. Here's a detailed guide on what to expect when applying for a mortgage, as well as tips and commonly asked questions.

The Mortgage Process

Firstly, it's essential to know what a mortgage is. A mortgage is a loan that you take out to buy a property. You'll pay back the loan over a set period, usually thirty years. Your interest rate and monthly payments will depend on factors such as your credit score, down payment, and loan type.

To apply for a mortgage, you'll need to gather some documentation. This includes your income, employment history, credit report, and bank statements. It's recommended that you get pre-approved for a mortgage before house-hunting. This means that a lender will review your finances and give you an estimate of how much you can borrow.

Once you've found a property, you'll need to submit an application for a mortgage. The lender will review your finances and the property's value and determine if you're approved for a loan. If you're approved, you'll receive a commitment letter, which outlines the terms and conditions of your mortgage.

Before your mortgage is finalized, there are a few things you'll need to do. This includes a home inspection, title search, and appraisal. The inspection ensures that the property is in good condition, and the appraisal confirms the property's value matches the sale price. The title search checks that there are no liens or legal issues with the property.

Once all of the above is completed, you'll sign a closing disclosure and pay your closing costs. This includes fees for services such as appraisal, title search, and attorney. Finally, you'll sign your mortgage documents, and the lender will release the funds to purchase the property.

Tips

Here are some tips to keep in mind when applying for a mortgage:

- Check your credit score before applying for a mortgage. A good score can help you secure a lower interest rate and better loan terms.

- Save up for a down payment. The more money you put down, the less you'll need to borrow, and the lower your monthly payments will be.

- Shop around for the best mortgage rates. Different lenders may offer better deals, so it's worth doing your research.

- Don't take on new debt while applying for a mortgage. This includes opening new credit cards or taking out a car loan. It can negatively impact your credit score and hurt your chances of getting approved.

Frequently Asked Questions

Here are some commonly asked questions about the mortgage process:

Q: How much of a down payment do I need?

A: It depends on the type of loan you're applying for. Conventional loans typically require a down payment of 20% of the home's purchase price. However, there are other loan options that require as little as 3% down.

Q: What if I have a low credit score?

A: You may still be able to get approved for a mortgage, but you'll likely pay a higher interest rate. It's recommended that you work on improving your credit score before applying for a mortgage.

Q: Can I get a mortgage if I'm self-employed?

A: Yes, but it may be more challenging to get approved. You'll need to provide more documentation, such as tax returns and business financial statements, to prove your income.

Q: What if I can't make my monthly payments?

A: Contact your lender immediately. They may be able to work out a payment plan or offer other solutions to help you avoid foreclosure.

In conclusion, the mortgage process can seem overwhelming, but it doesn't have to be. By understanding the steps involved and following the tips above, you'll be well on your way to owning your dream home.

Categories

Recent Posts

GET MORE INFORMATION